Since taking office in August 2023, Vanquis Banking Group CEO Ian McLaughlin inherited anything but a clean slate. Years of high costs, ongoing legal disputes, and strategic missteps had left deep scars. What followed was not a cautious adjustment, but a hard reset. He aggressively cut the cost base, dealt with legacy issues from the past, and did not shy away from painful decisions that had previously been postponed. Where the engine had once been sputtering beneath the surface, the company is now clearly cleaning house. Not without difficulty, but with a clear message: this is a bank that is no longer managing its problems, but solving them.

We already had this stock on our radar, but wanted to wait for the first-quarter results, as these would be decisive for the future share price direction. The results positively surprised us across the board. Perhaps even more important than the quarterly figures themselves is the fact that Vanquis maintained its full-year outlook. The bank still expects:

- further growth of the loan portfolio towards more than £3.3 billion

- a low double-digit return on tangible equity

- further improvement in the cost-income ratio

However, the market does not yet seem to recognize this and is still pricing in a scenario as if the recovery is not sustainable. Sharesunderten is taking advantage of this opportunity and is opening a position. We are buying 1,500 shares.

Chaos

For years, Vanquis found itself in a state of chaos, with problems piling up. The bank was flooded with claims from customers alleging that loans had been irresponsibly issued, often driven by claims management companies. The legal pressure became so intense that more than £130 million in exceptional charges had to be taken in 2024.

At the same time, the cost base had spiraled out of control. With a cost-income ratio approaching 90%, nearly every pound of revenue was being absorbed by inefficiencies, IT issues, and a bloated organization. On top of that came weak profitability. In 2024, the bank still reported a loss of £138 million, while return on equity was deeply negative.

The underlying issue was not only costs, but also risk management. The loan portfolio experienced relatively high losses and came under increasing pressure from regulators, further fueling the stream of claims. What emerged was a vicious cycle in which poor credit quality led to claims, claims led to higher costs, and higher costs led to even weaker results.

The situation was worsened by a lack of strategic focus. Growth was pursued without sufficient discipline, legacy operations remained in place for too long, and clear decisions were continuously postponed. For investors, this resulted in a loss of confidence.

Profile

Vanquis Banking Group is not a traditional bank, but a specialist lender focused on consumers who struggle to access financing through mainstream banks. The core of its business model lies in providing credit, particularly through credit cards, to customers with weaker or limited credit histories.

This segment, often referred to as non-standard or near-prime, offers higher margins but also requires stricter risk management. In addition to credit cards, the company is active in vehicle finance through its Moneybarn brand, primarily financing used cars.

Vanquis also has a rapidly growing second-charge mortgage division, allowing customers to borrow against the equity in their homes. On the funding side, the bank operates its own savings platform, attracting retail deposits that provide a relatively stable and low-cost funding source for the loan portfolio.

In addition, Vanquis is investing in digitalization and customer engagement through Snoop, a fintech app that uses open banking technology to help customers gain insight into their spending and save money. With this, the bank aims not only to provide credit, but also to play a broader role in the financial lives of its customers.

Results

In the first quarter of 2026, Vanquis Banking Group demonstrated that last year’s recovery is continuing. Gross interest-earning receivables increased by 4% to £2.93 billion. On an annual basis, growth reached 27%. Net receivables also rose by 4% to £2.80 billion.

Credit card operations in particular continue to perform strongly and have now delivered growth for the fourth consecutive quarter, supported by higher credit limit utilization, strong customer retention, and continued inflow of new customers. In addition, the second-charge mortgage division continued to grow towards approximately £680 million.

The net interest margin declined from 16.1% to 15.6%, but this fully aligns with management’s strategy. Vanquis is deliberately shifting toward lower-risk products that also generate lower interest income. More importantly, in our view, the risk-adjusted margin remained stable at 9.4%.

This demonstrates that the balance between return and risk remains healthy, and that the lower margins are largely offset by improved credit quality and a lower cost of risk.

Operational progress also remains visible. Management stated that Vanquis was once again profitable in the first quarter and remains on track to achieve a low double-digit return on tangible equity in 2026.

At the same time, the company continues to focus heavily on improving efficiency. Through the Gateway transformation program, Vanquis expects to achieve an additional £23 million to £28 million in cost savings during 2026 and 2027, supported by further automation, AI-driven customer service, and a more modern technology platform.

Despite strong growth, the balance sheet remains solid. The CET1 ratio stood at 15.9%, slightly lower than at the end of 2025 as capital is actively being deployed to support further loan portfolio growth. Nevertheless, Vanquis still maintains substantial buffers above required capital levels, keeping the balance sheet robust while allowing room for continued growth.

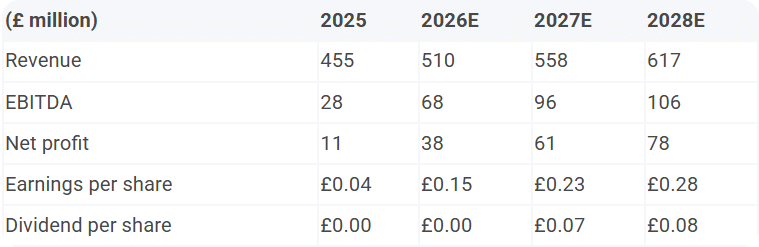

Forecasts

While 2024 and also 2025 were still dominated by write-downs, settlements, and legal costs, these burdens are now expected to be largely behind the company.

Revenue is expected to grow steadily, in line with management’s vision of pursuing growth without compromising risk discipline. Significant cost reductions have been implemented in recent years, which is reflected in strongly rising EBITDA and net profit. Earnings per share are following the same trend.

As profitability improves, dividend payments are also expected to resume from 2027 onward.

Conclusion

We are positive on Vanquis Banking Group because the company has managed to break free from a structurally weak period in a relatively short time and is now clearly demonstrating recovery. Yet this recovery is not reflected in the share price in any meaningful way.

While the bank returned to profitability in 2025, significantly improved its balance sheet, and greatly increased efficiency, the valuation still lags as if nothing has changed.

This is where the tension in the story lies. Vanquis operates in a niche market of so-called underserved customers, where demand remains structurally present while supply has declined due to stricter regulation and the disappearance of competitors. This creates room for controlled growth without immediate pressure on credit quality.

Management’s strategy is intentionally conservative: first strengthen credit quality further, then accelerate growth. At the same time, the company continues to reduce costs and scale up its core operations. Within this strategy, credit cards and second-charge mortgages stand out in particular, as growth accelerates and returns improve.

This is exactly the type of combination of growth and margins that can drive earnings higher over time.

But the real imbalance lies in the valuation. The stock trades well below tangible book value of GBX 169 per share and at an expected 2027 price-to-earnings ratio of just 5x.

Simply put, the market is still pricing in a scenario as if the recovery is not sustainable. Just returning to book value alone would imply upside potential of approximately 50%.

If current forecasts are even partially achieved, that discount appears difficult to justify. Nevertheless, the risks remain clearly present. This is a story that depends entirely on execution, credit discipline, and market sentiment.

And following the quarterly figures, we were certainly not the only ones reacting positively. Analysts at Berenberg issued a Buy recommendation today with a price target of GBX 165. This is not a firm that becomes enthusiastic based on a single quarterly update. It indicates that professional investors are increasingly seeing signs that Vanquis is undergoing a structural recovery.

Perhaps the most interesting aspect is sentiment itself. This is a heavily beaten-down stock where investor confidence still needs to be rebuilt gradually. That is precisely what creates the asymmetry: recovery in the numbers, silence in the share price.

Sharesunderten bases its view on the sum of the facts and sees a clear imbalance in the risk-reward profile emerging: a heavily punished valuation versus a company that is operationally recovering.

At current levels, this creates an attractive entry opportunity, with an initial price target of GBX 160, where re-rating could accelerate rapidly once the market truly starts believing in the recovery.

The author holds a position in Vanquis.